What Factors Influence Supply in Microeconomics?

TL;DR

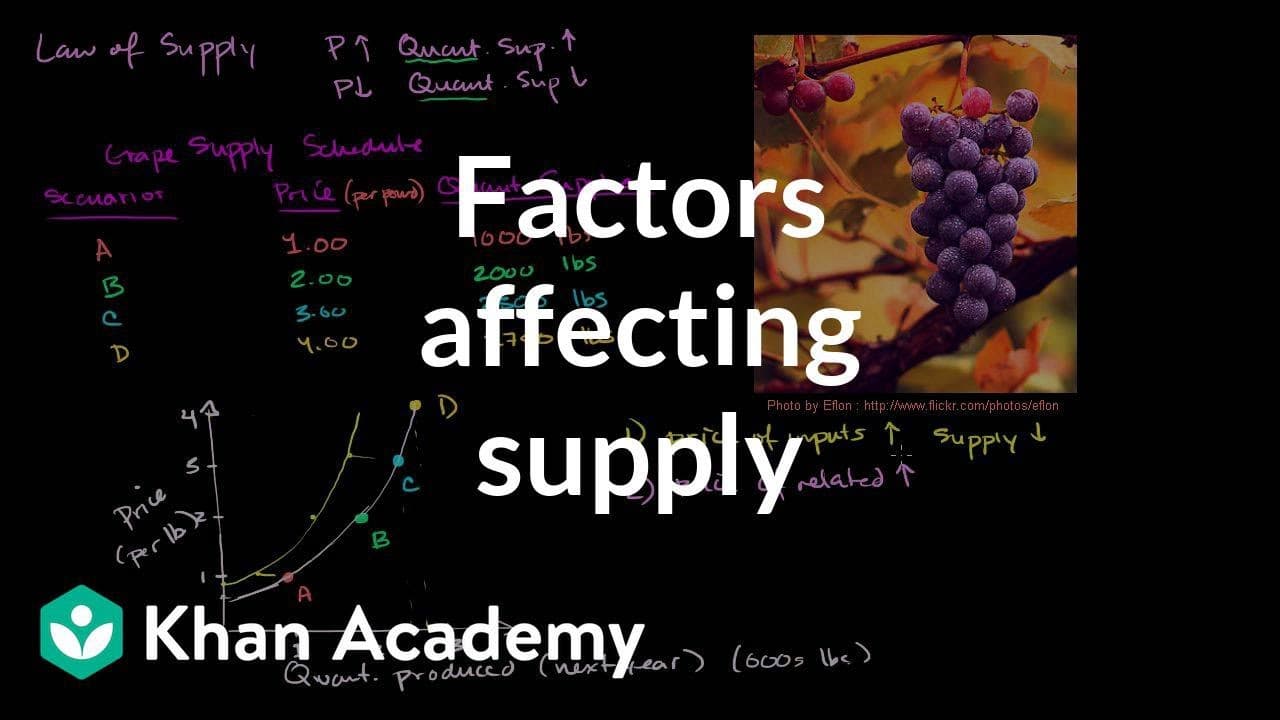

Supply is influenced by factors such as input prices, the number of suppliers, technological advancements, and expected future prices. Higher input costs generally decrease supply, while more suppliers and technology improvements increase it. If producers anticipate higher future prices, they may reduce current supply to sell later at a better price.

Transcript

In the last video, we introduced ourselves to the law of supply. And it was a fairly common sense idea that if we hold all else equal, that if the price of something goes up, there's more incentive for more producers to produce it or a given producer to produce more of it. And we saw that. As the price goes up, we moved along the supply curve, and ... Read More

Key Insights

- 🔬 The price of inputs, such as labor or materials, can significantly impact the supply of a product.

- 👋 Related goods, particularly substitutes for production, can influence the allocation of resources and affect supply.

- 🥺 The number of suppliers has a direct relationship with supply, with more suppliers leading to increased supply.

- 🇨🇷 Technological advancements can enhance supply by reducing costs or improving productivity.

Install to Summarize YouTube Videos and Get Transcripts

Explore YouTube Video Summarizer or Get YouTube Transcript Extractor

Questions & Answers

Q: How does the price of inputs affect the supply of a product?

When the price of inputs, such as labor or materials, increases, the cost of production rises. This makes it less profitable for producers to supply the product at a given price, leading to a decrease in supply.

Q: How do related goods impact supply?

Related goods, particularly substitutes, can influence supply. If the price of a substitute increases, producers may shift their resources towards that product, resulting in a decrease in supply of the original good.

Q: What role does the number of suppliers play in supply?

The number of suppliers directly affects supply. An increase in the number of suppliers leads to higher supply, while a decrease in the number of suppliers results in lower supply.

Q: How does technology impact supply?

Technological advancements can increase supply by reducing input costs or increasing productivity. This enables producers to supply more of a product at a given price, leading to an upward shift in the supply curve.

Summary & Key Takeaways

-

The law of supply states that as the price of a good increases, there is an incentive for producers to supply more. Conversely, if the price of inputs increases, producers may supply less.

-

The price of related goods, such as substitutes for production, can also influence supply. If the price of a substitute increases, producers may allocate more resources to that product, leading to a decrease in supply of the original good.

-

The number of suppliers directly affects supply. An increase in the number of suppliers leads to higher supply, while a decrease results in lower supply.

-

Technological advancements can increase the supply of goods by reducing input costs or increasing productivity.

-

Expected future prices can impact current supply. If producers anticipate higher prices in the future, they may withhold supply to sell at a later date.

Read in Other Languages (beta)

Share This Summary 📚

Summarize YouTube Videos and Get Video Transcripts with 1-Click

Try YouTube Summary with ChatGPT & Claude or YouTube Transcript Generator

Explore More Summaries from Khan Academy 📚

Summarize YouTube Videos and Get Video Transcripts with 1-Click

Try YouTube Summary with ChatGPT & Claude or YouTube Transcript Generator