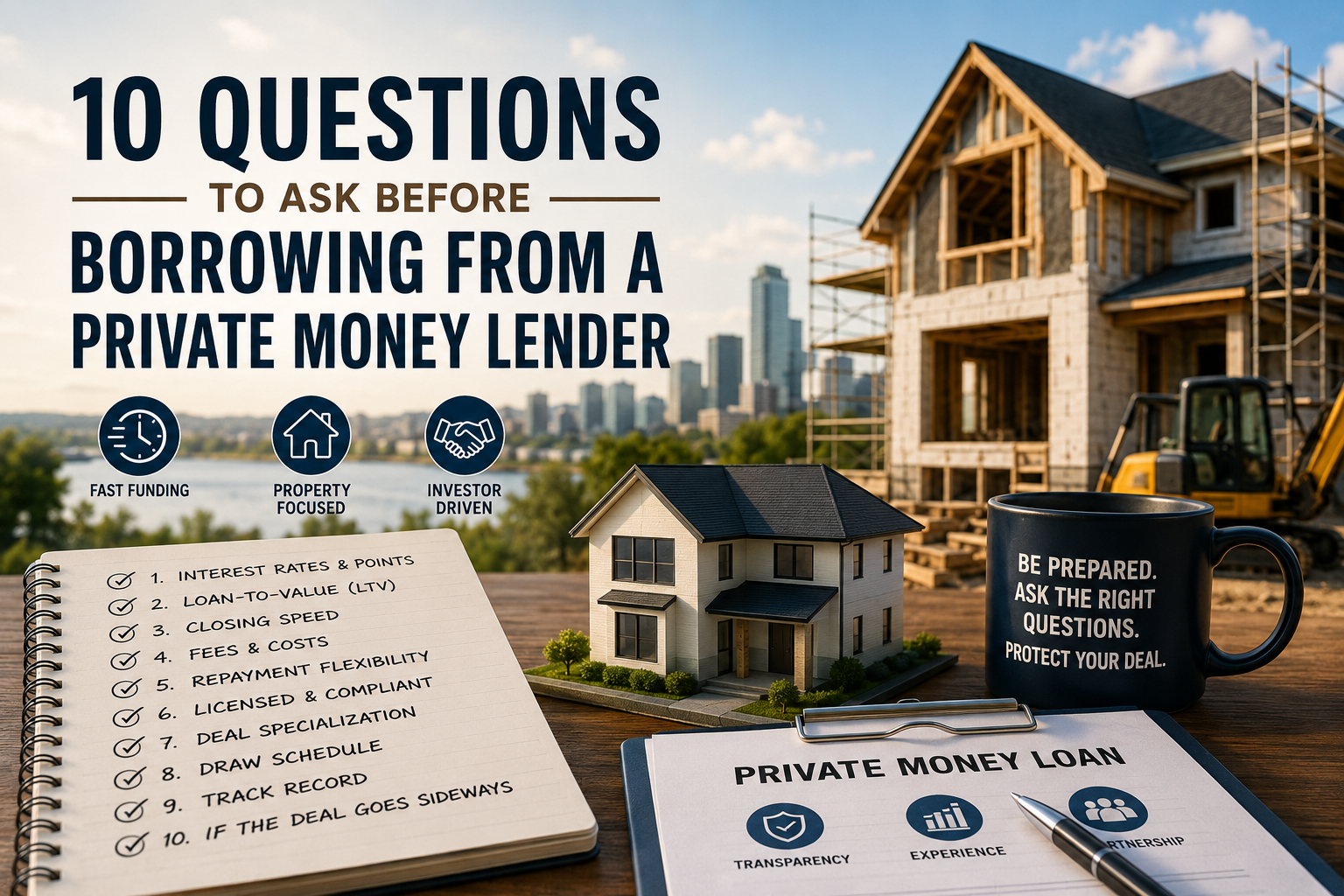

10 Questions to Ask Before Borrowing from a Private Money Lender

Jun 30, 2026

6 min read

2 views

Real estate investors often hit a wall when traditional banks say no — too slow, too much paperwork, too many conditions. That's where a private money lender steps in. These lenders move fast, focus on the property rather than your credit score, and can fund deals that banks won't touch.

But here's the catch: not all private lenders are created equal. The flexibility that makes private money lending so attractive is the same thing that makes it risky if you don't ask the right questions upfront. A bad deal can cost you thousands in unexpected fees, or worse, your property.

Before you sign anything, here are the 10 questions every borrower should ask.

1. What Are Your Interest Rates and Points?

This is the obvious one, but don't stop at the headline rate. Private money loans typically charge higher interest than conventional mortgages — often somewhere between 8% and 15%, depending on the lender, the deal, and your experience as a borrower. On top of that, most lenders charge "points," which are upfront fees calculated as a percentage of the loan amount (one point equals 1% of the loan).

Ask for the full breakdown: interest rate, number of points, and whether the rate is fixed or can change during the loan term. A lender quoting a low rate but tacking on five points might end up costing more than one with a slightly higher rate and fewer fees.

2. What's the Loan-to-Value (LTV) Ratio?

Private lenders base their decisions heavily on the value of the property, not just your financial profile. LTV tells you how much of the property's value the lender is willing to finance. Most private lenders cap LTV somewhere between 65% and 75% of the after-repair value (ARV) for fix-and-flip deals, though this varies.

Knowing the LTV upfront helps you figure out how much cash you'll need to bring to the table and whether the deal still makes financial sense once you factor in your down payment, renovation costs, and holding costs.

3. How Fast Can You Actually Close?

Speed is the main reason investors turn to private money lending in the first place. Banks can take 30 to 60 days; private lenders often promise 7 to 14 days. But promises and reality don't always match.

Ask the lender for examples of recent closings, not just their advertised turnaround time. Find out what could slow things down — appraisal delays, title issues, or internal approval processes. If you're competing for a property in a hot market, a lender who can't deliver on speed isn't actually solving your problem.

4. What Fees Are Involved Beyond Interest and Points?

This is where a lot of borrowers get caught off guard. Beyond interest and origination points, private lenders may charge:

Underwriting or processing fees

Appraisal or valuation fees

Legal or document preparation fees

Draw fees (for construction or rehab loans, charged each time you request funds)

Extension fees if you need more time to repay

Prepayment penalties if you pay off the loan early

Ask for a complete, itemized list of every fee associated with the loan before you commit. A reputable lender should be transparent about this without you having to dig.

5. What Happens If I Need More Time to Repay?

Private money loans are short-term by nature, usually ranging from 6 to 24 months. Renovation projects, however, rarely go exactly according to schedule. Permits get delayed, contractors fall behind, or the market shifts and your exit strategy needs to change.

Ask specifically what happens if you can't repay on time. Does the lender offer extensions? What do they cost? Is there a grace period, or does default kick in immediately? Understanding the lender's flexibility — or lack of it — before you're in a crunch can save you from a forced sale or foreclosure down the line.

6. Are You Licensed and Compliant in My State?

Private money lending regulations vary significantly from state to state. Some states require lenders to hold a specific license to originate loans, while others have looser requirements, especially for business-purpose loans (as opposed to owner-occupied residential loans, which fall under stricter consumer protection laws).

If you're working with a private money lender nationwide, this question becomes even more important, since the same company needs to comply with different rules in every state where they lend. Ask the lender directly about their licensing status and request documentation if needed. Working with an unlicensed or non-compliant lender can create legal headaches for you as the borrower, even if you didn't do anything wrong.

7. Do You Specialize in My Type of Deal?

Not every private lender funds every type of project. Some focus exclusively on fix-and-flip loans, others on rental property refinancing (DSCR loans), ground-up construction, or commercial bridge loans. A lender who mostly does single-family flips might not have the right loan structure — or risk appetite — for a multi-unit construction project.

Ask about their typical deal size, property types, and borrower profile. A lender who regularly funds projects like yours will likely have a smoother process, more realistic expectations, and better advice along the way.

8. What Is Your Draw Schedule for Renovation Funds?

If your loan includes funds for rehab or construction, the money usually isn't handed over all at once. Instead, it's released in stages — known as "draws" — as work is completed and verified. The structure of this draw schedule can make or break your project timeline.

Ask how many draws are typical, how long it takes to receive funds after requesting a draw, whether an inspection is required before each release, and whether there are fees per draw. Slow or overly bureaucratic draw processes can stall your renovation and eat into your holding costs.

9. What's Your Track Record and Reputation?

Anyone can put up a website and call themselves a private money lender. What matters is whether they actually have a track record of closing deals and treating borrowers fairly. Ask how long they've been in business, how many loans they've funded, and for references from past borrowers if possible.

Search for online reviews, check with local real estate investment associations, and ask other investors in your network if they've worked with the lender before. A lender with a long, consistent history in private money lending is generally a safer bet than one that's new or operates with little transparency.

10. What Happens If the Deal Goes Sideways?

No one likes to think about worst-case scenarios, but you need to understand them before you sign. What happens if the project goes over budget? If the property doesn't sell or refinance as planned? If you fall behind on payments?

Ask the lender to walk you through their default and foreclosure process step by step. Understand the cure period, communication process, and whether they're willing to work with borrowers facing temporary setbacks or whether they move straight to foreclosure. A lender who's upfront and detailed about this question is usually one who deals with borrowers honestly across the board.

Final Thoughts

Borrowing from a private money lender can be one of the smartest moves a real estate investor makes — it's fast, flexible, and focused on the deal rather than a long list of bureaucratic requirements. But that flexibility only works in your favor if you go in informed.

Asking these 10 questions won't just protect you from bad surprises; it'll also signal to the lender that you're a serious, prepared borrower, which can actually improve the terms you're offered. Whether you're working with a local lender or a private money lender nationwide, the goal is the same: find a partner who's transparent, experienced, and aligned with the success of your project — not just the size of their next fee.

Take the time to ask the hard questions now. It's a lot cheaper than learning the answers the hard way.

Comments

Written by Simplending Financial

Simplending Financial is a trusted private lending firm offering customized financing solutions for real estate investors.