How to Use Markov Models for Quant Trading

TL;DR

Quant trading strategies differ from traditional methods by using Markov models to analyze market states. These models classify market conditions into bull, bear, and sideways states based on historical data and probabilities. By leveraging AI and specific prompts, traders can automate these strategies, enhancing accuracy and consistency in decision-making.

Transcript

I've realized something about trading. Average people who are trying to do day trading, even all the way up to professionals doing trading, they do it completely different than how hedge funds do it. Now, I want to tell you something that I've learned recently that completely shattered my view of trading. And that is that quants are not using trend... Read More

Key Insights

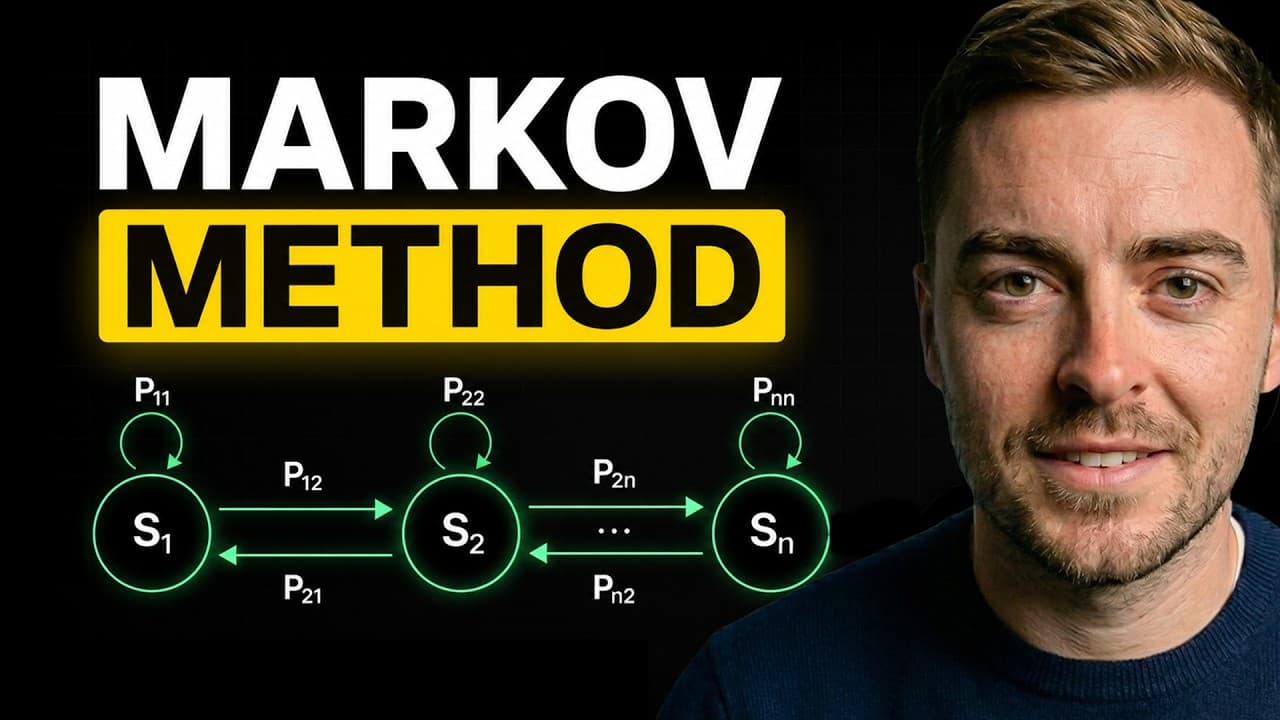

- Quant trading uses Markov models to classify market states into bull, bear, and sideways based on 20-day returns.

- The Markov property emphasizes that only the current state influences future market conditions, not historical data.

- A 3x3 transition matrix calculates the probability of market state transitions, aiding in prediction and strategy formulation.

- The concept of 'stickiness' describes the likelihood of a market state persisting into the next day, guiding trade decisions.

- Multi-day forecasts are generated by squaring the transition matrix, but long-term predictions tend to lose significance.

- Trade signals are generated by subtracting bear probability from bull probability, indicating the strength and direction of trades.

- Walk-forward backtesting prevents strategies from being biased by future data, ensuring more reliable backtesting results.

- The hidden Markov model removes subjective state labels, instead relying on pattern recognition to define market states.

Install to Summarize YouTube Videos and Get Transcripts

Explore YouTube Video Summarizer or Get YouTube Transcript Extractor

Questions & Answers

Q: How do quant traders use Markov models?

Quant traders use Markov models to classify market states into bull, bear, and sideways based on a 20-day return analysis. These models help in predicting future market conditions by focusing on the current state rather than past trends. A 3x3 transition matrix is used to calculate probabilities of state transitions, aiding in strategy formulation and decision-making.

Q: What is the Markov property in trading?

The Markov property in trading emphasizes that only the current market state influences future conditions, not historical data. This principle is fundamental in quant trading strategies, where the focus is on the present state to predict future movements. This approach contrasts with traditional methods that often rely on historical trends and patterns.

Q: How is a 3x3 transition matrix used in quant trading?

In quant trading, a 3x3 transition matrix is used to calculate the probabilities of transitions between market states: bull, bear, and sideways. Each row represents the current state, while each column represents possible future states. This matrix helps traders predict the most likely market condition for the next day, enhancing strategy accuracy.

Q: What does 'stickiness' mean in market states?

Stickiness refers to the likelihood of a market state persisting into the next day. For example, if a market is currently in a bull state, stickiness indicates the probability that it will remain in a bull state the following day. This concept is crucial in quant trading, as it helps traders assess the persistence of market trends and make informed decisions.

Q: How are multi-day forecasts generated in quant trading?

Multi-day forecasts in quant trading are generated by squaring the transition matrix, which involves multiplying the matrix by itself. This process provides probabilities for market states over multiple days. However, as the forecast period extends, the significance of these probabilities may diminish, making long-term predictions less reliable.

Q: What is walk-forward backtesting?

Walk-forward backtesting is a method that prevents trading strategies from being biased by future data. Unlike traditional backtesting, which applies strategies to past data, walk-forward backtesting recalculates strategies daily. This approach ensures that strategies are tested in a realistic manner, providing more reliable and accurate results for traders.

Q: How does the hidden Markov model improve trading strategies?

The hidden Markov model refines trading strategies by removing subjective state labels and relying on pattern recognition to define market states. This model analyzes price history without pre-assigned labels, identifying patterns and trends that indicate market conditions. By doing so, it enhances the accuracy and objectivity of quant trading strategies.

Q: What role does AI play in quant trading strategies?

AI plays a crucial role in automating and enhancing quant trading strategies. By using specific prompts and models like Claude Code, traders can integrate complex mathematical models into their trading systems. AI helps in processing large datasets, executing strategies with precision, and adapting to changing market conditions, ultimately improving trading performance and decision-making.

Summary & Key Takeaways

-

Quant trading strategies utilize Markov models to define market conditions into bull, bear, and sideways states. This method relies on historical data and probabilities, differing from traditional trading by focusing on the current state rather than past trends. By leveraging AI, traders can automate these strategies, ensuring more accurate and consistent decision-making.

-

The Markov property in quant trading emphasizes the importance of the current market state over historical data. A 3x3 transition matrix is used to calculate the probability of state transitions, assisting in predicting future market conditions. This approach enhances the precision of trading strategies by focusing on calculated probabilities rather than trends.

-

Trade signals in quant trading are derived by subtracting bear probability from bull probability, indicating the strength and direction of trades. Multi-day forecasts are created by squaring the transition matrix, although long-term predictions may lose significance. The hidden Markov model further refines these strategies by removing subjective state labels.

Read in Other Languages (beta)

Share This Summary 📚

Summarize YouTube Videos and Get Video Transcripts with 1-Click

Try YouTube Summary with ChatGPT & Claude or YouTube Transcript Generator

Explore More Summaries from Lewis Jackson 📚

Summarize YouTube Videos and Get Video Transcripts with 1-Click

Try YouTube Summary with ChatGPT & Claude or YouTube Transcript Generator